Business Adoption of AI in Israel: Initial Insights from a First-of-Its-Kind Survey

A new IDI analysis of a Central Bureau of Statistics survey finds 28% of businesses in Israel used AI in the past six months as part of their business activity. In terms of employees, the proportion is even higher, with 32% of employees working in businesses in which AI is being used.

Photo by Canva

Artificial intelligence (AI) is now seen as one of the main fundamental technologies of the current era—similar to electricity in the 19th century or the internet at the end of the 20th century (OECD, 2025). As noted in a previous review by the Israel Democracy Institute (Aviram-Nitzan and Shebson, 2025), it has the potential to bring about structural change to various aspects of the economy and the labor market, driving productivity and growth on the one hand, and inequality on the other. In particular, in terms of the labor market, the research literature indicates two main possibilities for the impact of AI. One is that of complementarity between AI and human labor. In this scenario, task automation, particularly routine and technical tasks, frees up employees to engage in tasks that have not been automated and that may increase wages and job satisfaction. By contrast, the second possibility is the substitutability of employees by AI. In this scenario, the scale of tasks in which humans are replaced is large enough to make the human worker redundant, and ultimately to lead to significant levels of technological unemployment.

In response to the COVID-19 crisis, the Israeli Central Bureau of Statistics (CBS) developed an alternating chapter of its monthly Business Tendency Survey, facilitating examination of current and relevant issues for policymakers using a relatively large sample of businesses (CBS, 2025). In June, after consultations with several institutions—including the Israel Democracy Institute, the Israel Innovation Authority, and the Bank of Israel—the CBS produced a questionnaire aimed at examining the use of AI by businesses. This survey adds several new aspects to the existing discourse: First, it asks about actual usage patterns, as opposed to potential usage. Second, it reflects the perspective of businesses and not just employees, as the respondents are senior managers—thus having a broader view of the business, as well as better insights related to certain aspects of adoption (such as an understanding of the barriers to adoption). Third, it asks directly about the impact of AI on employment and the performance of tasks previously carried out by employees in the business.

The analysis below seeks to offer preliminary insights from this survey, in order to help shape policy on this subject. It is also based on major previous studies on the subject and provides a comparative view both within the business sector between different industries in Israel, and in relation to similar business surveys in other countries.

We begin by examining the following basic question: To what extent is AI used in the business sector in Israel? The surveyFor details about the methodology of the CBS survey and that of the international surveys to which we are comparing, see the Appendix, which is available in Hebrew upon request. indicates that 28% of businesses in Israel used AI in the past six months as part of their business activity. In terms of employees, the proportion is even higher, with 32% of employees working in businesses in which AI is being used.

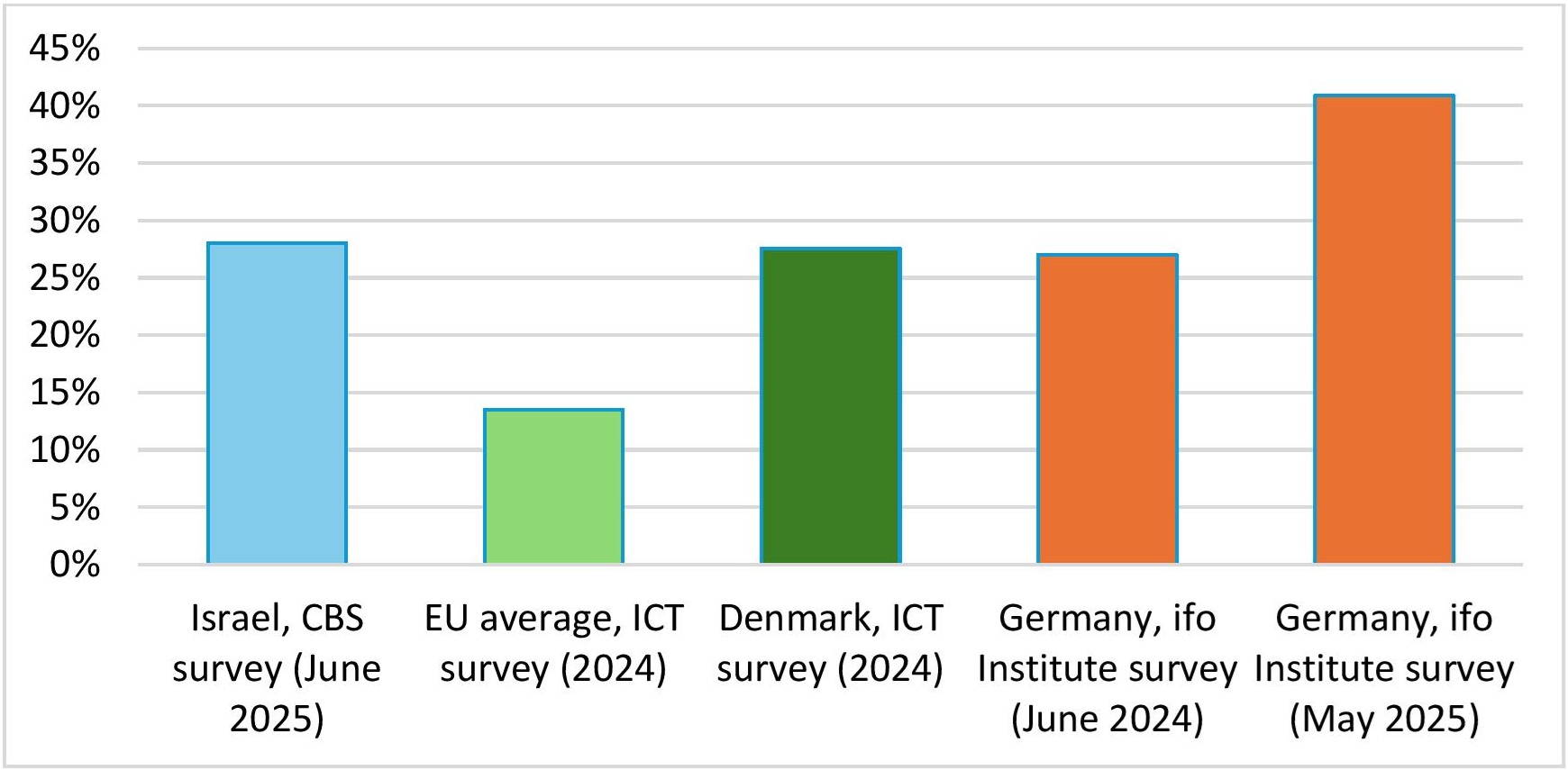

Figure 1 presents an international comparison of these findings. The data on all EU countries are from a survey on the use of technologies in businesses (referred to as the EU ICT survey) conducted in 2025, in which businesses were asked about the use of AI in 2024 (data was mostly collected on the first half of that year). The figure shows that AI use in Israel as reported in June 2025 is similar to the leading country in the European Union in 2024 (Denmark) and is double the EU average. To complete this picture, given the accelerated technological developments in this field, it is also critical to obtain an up-to-date perspective. To this end, we have also added a similar finding from a question asked in a German business survey conducted by the ifo Institute in May 2025. This shows that at a more recent point in time, the level of adoption in Israel was lower than in a country with a relatively high technological level such as Germany (28% versus 41% of businesses, respectively). For the sake of comparison, the result from the same German survey from June 2024 is also presented, which indicates the rate of technological change—a 1.5-fold increase in the level of use (from 27% to 41%).If we apply this rate of adoption to the EU average, it will have reached 20% in 2025, such that the level of usage in the Israeli business sector would still be higher. However, due to the non-linear pace of technological progress, such forecasts should be approached with caution. Another point of comparison to the German data is the percentage of businesses that used artificial intelligence in the EU ICT survey, which was conducted during the first half of 2024 in Germany. This rate stands at about 20%, compared to 27% from the ifo survey conducted in June 2024. According to this finding, too, Germany is at the upper part of the distribution of AI use in the European Union. The discrepancies between the surveys can be attributed to the different times at which they were carried out and the different methodologies used. In addition, even if we standardize the ifo Institute survey data for 2025 using the relative difference in 2024 between the two surveys (which reduces the estimate by around 25%), the German figure would still be slightly higher than the Israeli figure (31% vs. 28%). It is important to note that since these international surveys are similar but not identical in terms of their timing and survey methodology, the comparisons should be treated with caution (additional information on the methodology is available in Hebrew appendices upon request). At the same time, they may offer an approximation of the relative state of adoption of AI in Israel at this time.

Figure 1. Use of AI in businesses in Israel compared to other countries

Source: Processing of data from the CBS survey, the EU ICT survey, and the German ifo Institute survey

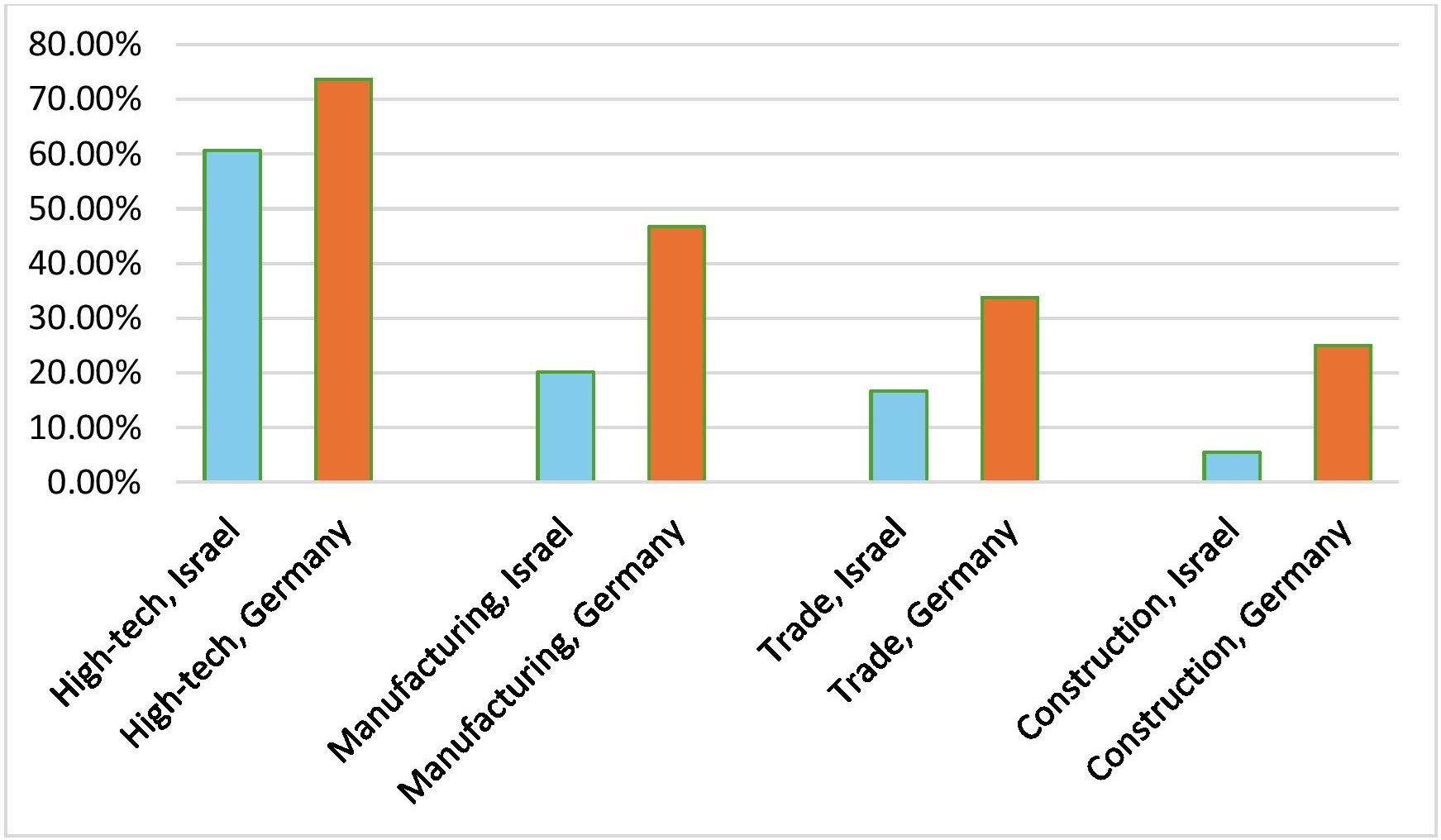

Of course, the disadvantage of a statistical average is that it conceals possible variations across different business sectors. An analysis of the various industries studied in the survey shows that this is indeed the case regarding the use of AI. As can be seen in Figure 2, the level of use in knowledge-intensive industries, led by high-tech, stands at nearly three times that of more traditional industries such as manufacturing, trade, and construction. It could be argued that this is a global characteristic of traditional industries, according to which the manual nature of their work processes and the lower level of technology they deploy (on average) result in a lower potential for the use of AI (Calvino et al., 2024). However, Figure 2 shows that even when comparing the same industries at a similar point in time in Israel and Germany (June 2025 and May 2025, respectively), there are differences by a ratio of between 2 and 4.

Figure 2. Share of businesses using AI, by industry (as % of all businesses in the industry)From the ifo Institute survey, we used the IT services industry as a comparison for Israel’s high-tech industry. In Israel, the high-tech sector also includes the high-tech manufacturing industry as well as financial services (according to the CBS, the AI usage patterns in these knowledge-intensive industries were found to be similar; the however, they are too small to be published separately, and are therefore reported together with the high-tech industry).

Source: Processing of data from the CBS survey and the German ifo Institute survey

These discrepancies can be linked to many findings regarding the dual structure of the Israeli economy, which differentiates the high-tech sector from the rest of the economy (see, for example: Bank of Israel, 2019), and in particular, the “digital divide” of non-high-tech industries (Be’ery and Esperanza, 2021; Golstein-Galperin et al., 2023). As far back as 2020, an OECD study on AI usage found that the usage gaps between the high-tech industry and other industries in Israel were among the largest of the countries in the comparison (Calvino and Fontenelli, 2023). All these findings raise concerns that AI could deepen the divide between industries in Israel.

Analyses of the potential impact of AI on the Israeli economy predict significant levels of job and employee replacement. For example, a Taub Center study (Debowy et al., 2024) found that around 23% of workers in Israel are at risk of being replaced by AI, because they have a high level of exposure and a low level of complementarity in relation to this technology. A Bank of Israel forecast (Bank of Israel, 2025), which focuses on the effects of generative AI, also produced a similar estimate of 20% of employees in Israel who are expected to be replaced. At the same time, these studies predict that 30%–50% of employees are expected to benefit from technological complementarity. Regarding the two types of impact, there is a great deal of variation between industries, with certain industries being particularly vulnerable to substitutability, especially knowledge-intensive industries that have stronger populations in the labor market (such as the finance industry).

The CBS survey provides an initial assessment of the current situation in this regard.It should be noted that the CBS survey focuses on the business sector, while the studies on the potential impact of artificial intelligence examine all sectors of the economy, including the public sector. In what follows, however, we compare similar industries in a way that eliminates concerns in this regard. Inspired by the research described, there are two questions in the survey that address the replacement of human roles with artificial intelligence, and which were directed only to businesses that reported the use of AI. The first question concerns the transfer of tasks to AI. In this sense, AI is already having a significant impact on the allocation of tasks in businesses: 60% of businesses (in terms of employees)Here we have used a report of CBS data expressed in terms of employees, that is, the proportion of relevant responses presented in a way that gives weight to the size of the business. These data are more suitable for discussing the questions of the impact on employment, both because of the relevance of the scope of employment that may potentially be affected, and because of the fact that, according to the CBS, these data are more appropriate in cases relating to a small percentage of respondents. that reported using AI responded that certain tasks in the business that were previously performed by humans are now performed by AI. Of these 60%, most said that this relates to “routine and technical tasks only” (44%); however, there is already a significant share (16%) reporting that artificial intelligence also performs “tasks that require thinking".In order to give the equivalent proportions of the entire population of businesses surveyed (both users and non-users), these data must be weighted by the proportion of users, which, as recalled, stands at about 30%. This reduces the incidence of job replacement to around 15%–20% of businesses (depending on analysis by employees/employment).

The second question goes a step further and examines whether changes in task allocation are already being reflected in the business’s workforce. Here, the impact reported is significantly lower, though not negligible: Of the businesses that reported using AI, 9% (in terms of employees) say that it has had an impact on the number of employees in the business—around 5% say that it has had a “soft” effect of leading to the recruitment of fewer new employees, while the rest say that it has actually reduced the existing number of employees. At the same time, there is great variation between industries in this context—the trade sector at one extreme, reporting a lack of impact on its workforce, while in high-tech, some 10% of businesses (in terms of employees) report a reductional effect on employment (of all types). It is important to note that in the CBS survey, the reporting is of impact on workforce at the level of individual businesses, and thus the data in terms of employees is the percentage of workers employed in businesses that reported such an impact; however, this does not necessarily mean that they are all affected in the same manner. Consequently, this finding from the CBS survey should be understood as indicating the existence of substitutability among this population of workers, but not the actual substitutability of all of that share of workers.

In order to compare these data to the potential impact on worker replacement found by the Taub Center study (Debowy et al., 2024), we weighted the percentage of employees working in businesses that reported an impact on employment with the percentage of businesses that use AI (as noted, the question about the impact of AI on employment was directed only to businesses that reported using it). The findings are presented in Table 1. It is evident that although the CBS survey already shows significant effects on the characteristics of employment in businesses—mainly in terms of reallocation of tasks, with a smaller impact on the size of the workforce—this current state of affairs is still far from the potential impact. For example, though businesses employing around 6% of workers in the high-tech industry—not an insignificant share—reported a reduction in workforce or non-recruitment of new employees due to the use of AI, this is still significantly lower than the estimated potential for substitutability (47%). However, a single survey at one point in time is not sufficient to provide solid conclusions: Since AI technology is developing at a rapid pace, and as we have seen, the characteristics of its adoption are dynamic over time, it is certainly possible that we will see even stronger effects on the workforce in the future.

Finally, it is evident that the impact on employment in the high-tech sector is greater. It is likely that this pattern reflects not only the faster rate of adoption in technology industries, but also the higher level of substitutability in technological occupations such as software development. At the same time, the development of AI is expected to create new demand in the high-tech industry (Bank of Israel, 2025). It is important to continue to examine the cumulative effect of these conflicting influences on the growth of the high-tech industry, both in terms of productivity and output, and in terms of employment.

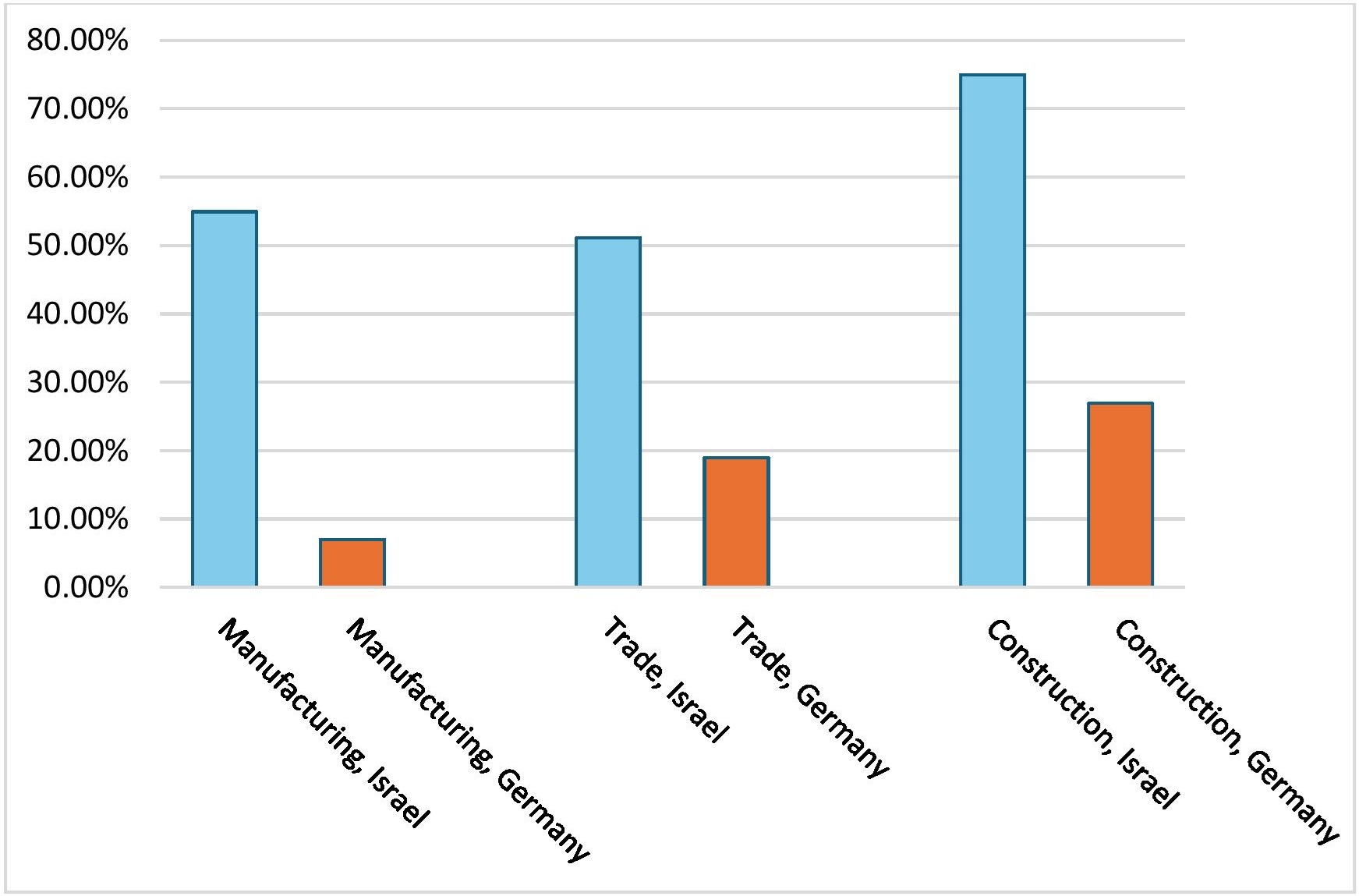

Table 1. Replacement of workers by AI—comparison of potential for substitutability found by Taub Center assessment with actual reporting in the CBS survey, by industry

| IndustryThere are certain differences in the definitions of industries between the two publications: As stated in the note above, in the CBS survey, the high-tech industry includes not only high-tech services, but also elite industry and the finance industry. In contrast, the Taub Center’s analysis uses the uniform classification of industries in the Israeli economy. For the purposes of the present comparison, we took the substitutability potential data for the “Information and Communication” (J) sector as an approximation for comparison with the high-tech and finance sector used by the CBS, and the “Manufacturing” sector (C) for comparison with the manufacturing industry sector in the CBS publication (even though it does not include elite industry). | Proportion of workers in businesses that reported a reductional impact on manpower in the CBS surveyThe weighting is required in order to adjust the estimate of those reporting a reduction in employment for the businesses comprising the entire population of businesses in the various industry sectors (both users and non-users). In the CBS survey, reporting about the impact on the workforce is given at the level of individual businesses, and therefore the figure in terms of employees relates to the share of workers employed in businesses that reported such an impact; however, this does not mean that all employees in those businesses are at risk of being affected. | Proportion of workers at high risk of being replaced (Debowy et al., 2024) |

| Construction | 0.40% | 8% |

| Manufacturing | 3% | 14% |

| Trade | 0% | 15% |

| High-tech | 6% | 47% |

Source: Processing of data from the CBS survey and from Debowy et al. (2024)

The survey asked businesses about businesses' intention to use AI over the next six months. Looking ahead, the share of businesses that expect to use AI in the next six months is similar to the share that reported use in the previous six months (27% and 28%, respectively). However, in terms of employees, there is a certain increase when looking toward the future (around 36%, compared to 32% over the last six months), which could indicate an expectation of more significant use in large businesses.

For this question about the future, respondents were also given the “Don’t know” response option, which was selected by 29% of businesses. Not knowing is not only a statement of fact but can also relate to knowledge as a possible barrier for businesses in the implementation of AI. Thus, in a follow-up question for the businesses that responded “Don’t know” or “No” regarding their expected future use of AI, they were asked why they are not planning such use. 71% responded that this is due to the lack of relevance of AI to their activity. Among the others, the single most significant barrier cited was “lack of knowledge about AI capabilities.” The share that gave this response was especially large among businesses in traditional industries.

Figure 3. Share of businesses in traditional industries that reported that AI is not relevant to their business, by industry (as % of all businesses in the industry)The question about barriers was asked by the CBS only of businesses that responded that they would not use artificial intelligence in the next six months or that they did not know whether they would do so. Against this background, the data for Israel in the figure weights the share of businesses that answered that artificial intelligence is not relevant to them by the share of businesses that were asked to respond to this question in the first place, in order to give an estimate for the overall population of businesses. This was done in order to create a more precise comparison with the data from Germany.

The CBS survey on the use of AI in business opens a window, the first of its kind, onto the actual usage of this central technology in the business sector in Israel. The survey indicates significant penetration of AI technologies into the business sector in Israel, but also large differences between industries and great variation in the extent of implementation. Alongside widespread adoption in the high-tech industry, there is a reluctance or delay in adoption in traditional industries, which may also reflect a lack of knowledge on the subject. This finding reinforces recommendations previously published by the Israel Democracy Institute, in cooperation with the Ministry of Economy and Industry, according to which innovation policy in Israel should focus not only on the development of new technologies in the high-tech industry, but also on the implementation of existing technologies throughout the rest of the economy (Golstein-Galperin et al., 2023).

In terms of the employment market, the survey shows that the impact of AI is already evident in the changes in how tasks are distributed within businesses: In a significant quantity of businesses, certain tasks that were previously performed by humans are now being carried out by AI. There is also reduced demand for workers, albeit on a smaller scale than the estimates given in previous studies regarding the potential replacement of employees by AI. It is possible that the discrepancy between the share of businesses reporting the use of artificial intelligence for tasks previously performed by employees and the share of businesses reporting a change in the number of their employees may be due to processes of complementarity as opposed to substitutability. At this stage, the complementarity effect seems to be more dominant, with AI tending more to complement rather than replace employees. As a result, the structure and nature of the allocation of work tasks is changing at a faster rate than the size of the workforce is. However, the rapid evolution of this technology and the dynamic characteristics of its use require that this insight be restricted solely to the present point in time, as there is considerable uncertainty about future developments. These findings underscore the importance of continuing to systematically monitor developments in real time.

At the same time, the early indications of impact on employment are already signaling the need for major policy reforms in the field of labor market policy. Recommendations in this direction were made in a previous IDI report (Aviram-Nitzan and Shebson, 2025), including a significant expansion of training for existing employees by employers and the development of life-long learning policies, in a way that will enable necessary adjustments to be made in the rapidly changing labor market. Alongside this, action must be taken to adapt the education system to the age of AI, and in particular to the development of various capabilities related to the subject—both those that support the development of high-quality AI usage skills, and those that complement such usage, such as critical thinking.

Finally, in all policy efforts, the difference in AI adoption rates between the high-tech industry and the more traditional industries, as well as between stronger and more vulnerable populations, should be considered. This will ensure that the potential of AI for driving economic growth can be realized in an inclusive manner, both maintaining the leading edge of the Israeli high-tech sector and its contribution to the economy and employment, and ensuring that no-one is left behind.

* Many thanks to Dr. Daniel Roash of the CBS for leading both the execution of the survey and the collaboration on designing the survey content, as well as for making the data available for this review. Thanks also to the staff at the Israel Democracy Institute for their contribution to this publication, and in particular, to Daphna Aviram-Nitzan for her feedback and helpful comments; to Eitan Ben-Eliya for his assistance with analysis and with editing; and to Zak Hirsch and Roe Kenneth Portal for their collaboration on designing the questionnaire and analyzing findings.