The Financial Situation of Evacuees in Israel

A special analysis of the situation among evacuees from the north and south of Israel, based on an extensive survey conducted among a nationally representative sample of workers who were in employment immediately before the outbreak of the Iron Swords war.

photo by Dor Pazuelo/Flash90

This report offers a special analysis of the situation among evacuees from the north and south of Israel, based on an extensive survey conducted among a nationally representative sample of workers who were in employment immediately before the outbreak of the Iron Swords war. The survey was carried out in order to assess the employment situation and financial situation of Israelis who were working prior to the war, with a special focus on the population of evacuees. The questionnaire covered five main topics related to the impact of the war on the financial circumstances of salaried and self-employed workers: employment status and work hours; individual and household income; liquidity; loans and overdrafts; and payments for housing.

To gain a better understanding of the situation among evacuees, we increased the sample size of this population group to an extent greater than its relative share of the overall population. Given the limited size of the evacuee population, the sample size is not large—90 respondents from locations that were evacuated; of these, 48 were from locations in the north, and 42 from locations in the south. Due to this relatively small sample size, the maximum sampling error was relatively large: ±8.67% at a confidence level of 90%.

Questionnaire design and survey analysis were conducted by the research staff at the Center for Governance and the Economy, with consultation and support from the Viterbi Family Center for Public Opinion and Policy Research at the Israel Democracy Institute. Data collection was carried out by CI Marketing Information between December 15, 2024 and January 5, 2025, some 15 months after the beginning of the Iron Swords war, with 992 men and women interviewed in Hebrew and 244 in Arabic.

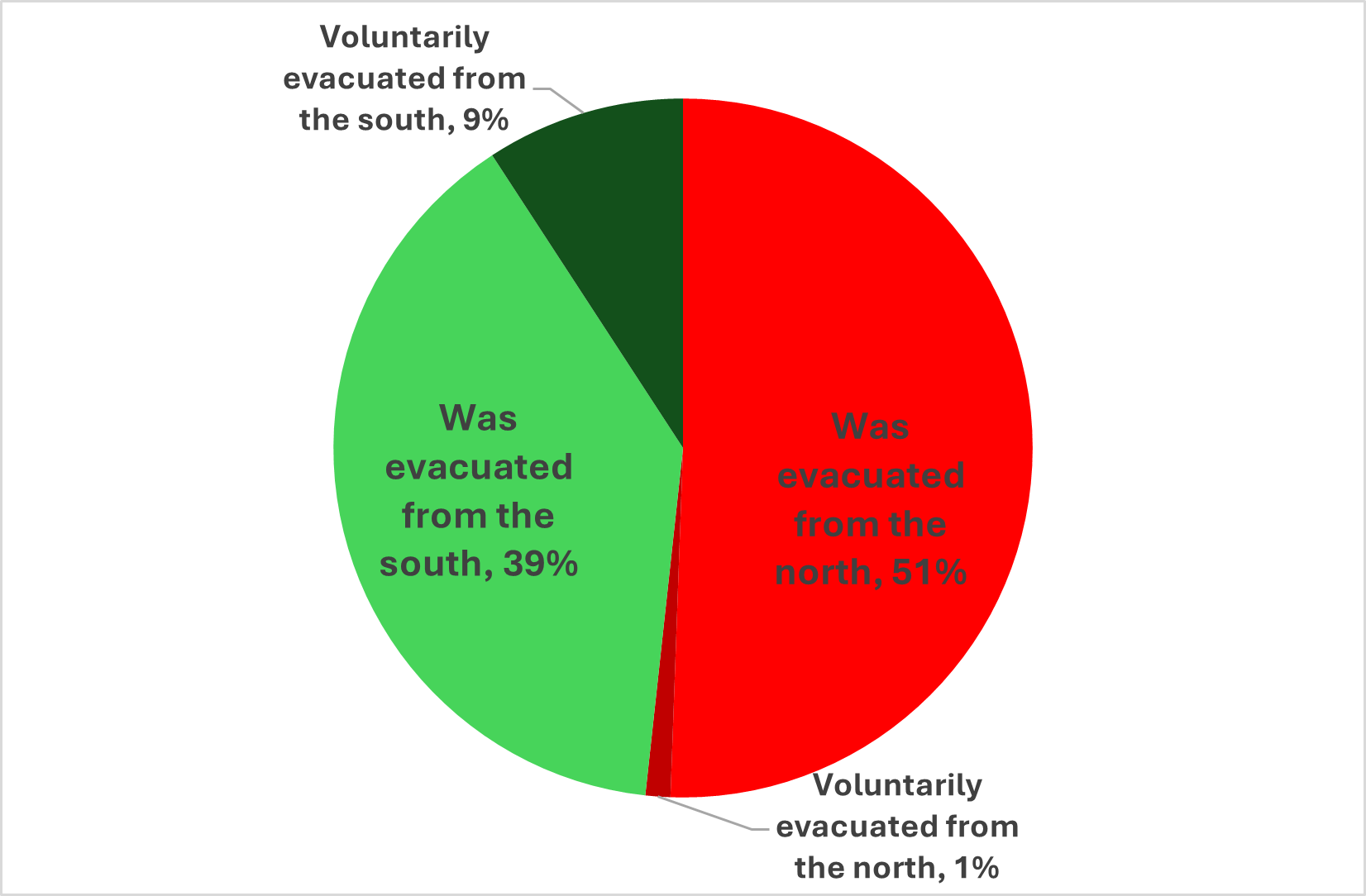

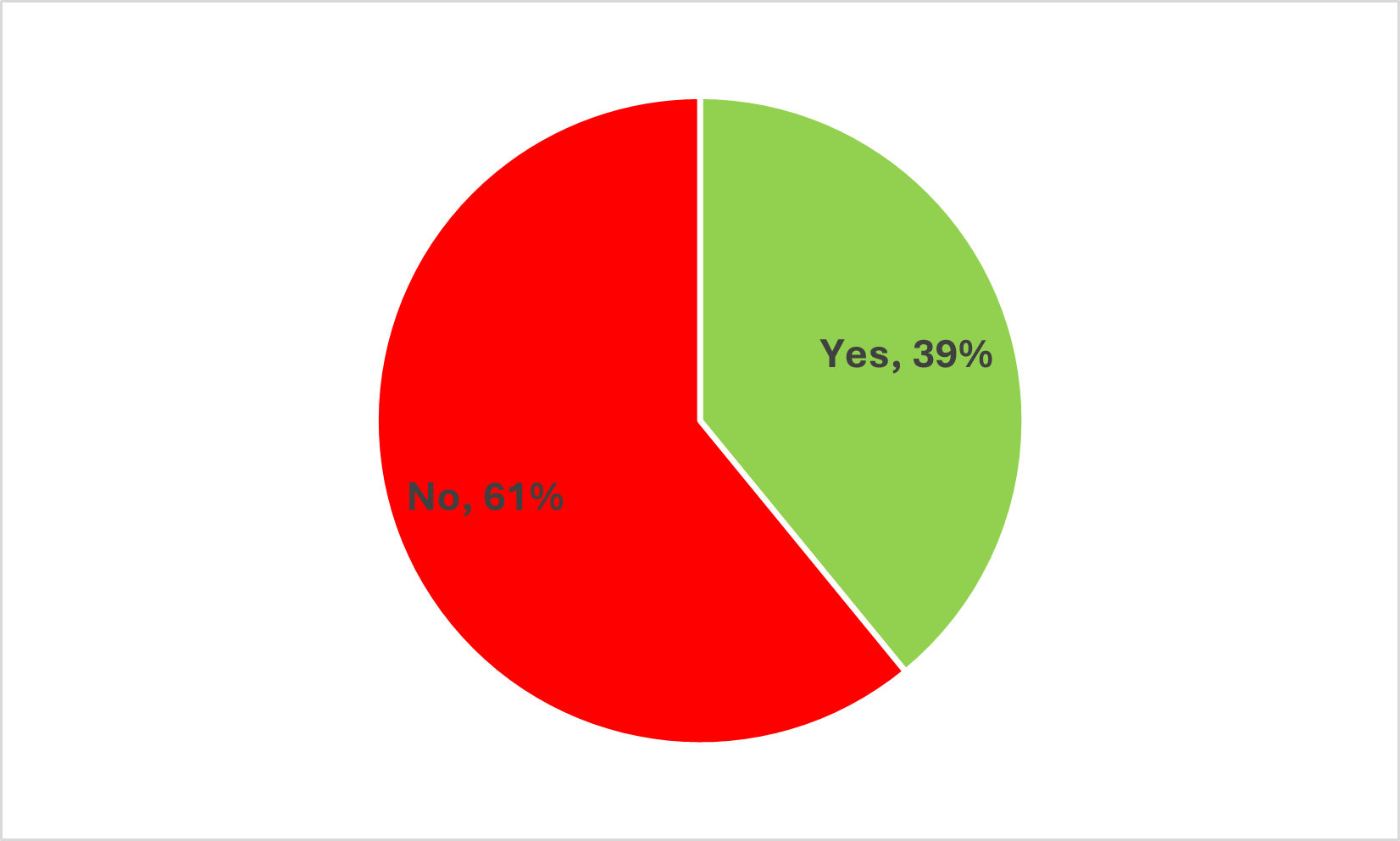

Among the evacuees, 90% were evacuated from their homes—51% from homes in the north, and 39% from homes in the south. 10% of respondents evacuated their homes of their own accord, the majority of them (95%) from the south. Most of the respondents (61%) had yet to return to their homes at the time of the survey, while just 39% had returned home.

Of those who had returned to their homes, 91% were from localities in the south, and just 9% were from localities in the north. Looking at each region separately, 76% of evacuees from the south had returned home, while 24% had yet to return; and just 7% of evacuees from the north had returned home, while 93% were still living elsewhere.

Figure 1. Were you evacuated from your home or did you evacuate your home due to the war?

Figure 2. Have you returned to your home?

We should note that the period during which the survey was carried out, from mid-December 2024 to early January 2025, came after the ceasefire agreement with Lebanon but before the current deal for the release of the hostages in Gaza, which also includes commitments to end the war and reduce the presence of IDF troops. It is reasonable to assume that these developments would have influenced the interviewees’ general outlook and level of optimism, particularly among evacuees from the south, and particularly regarding questions looking toward the future.

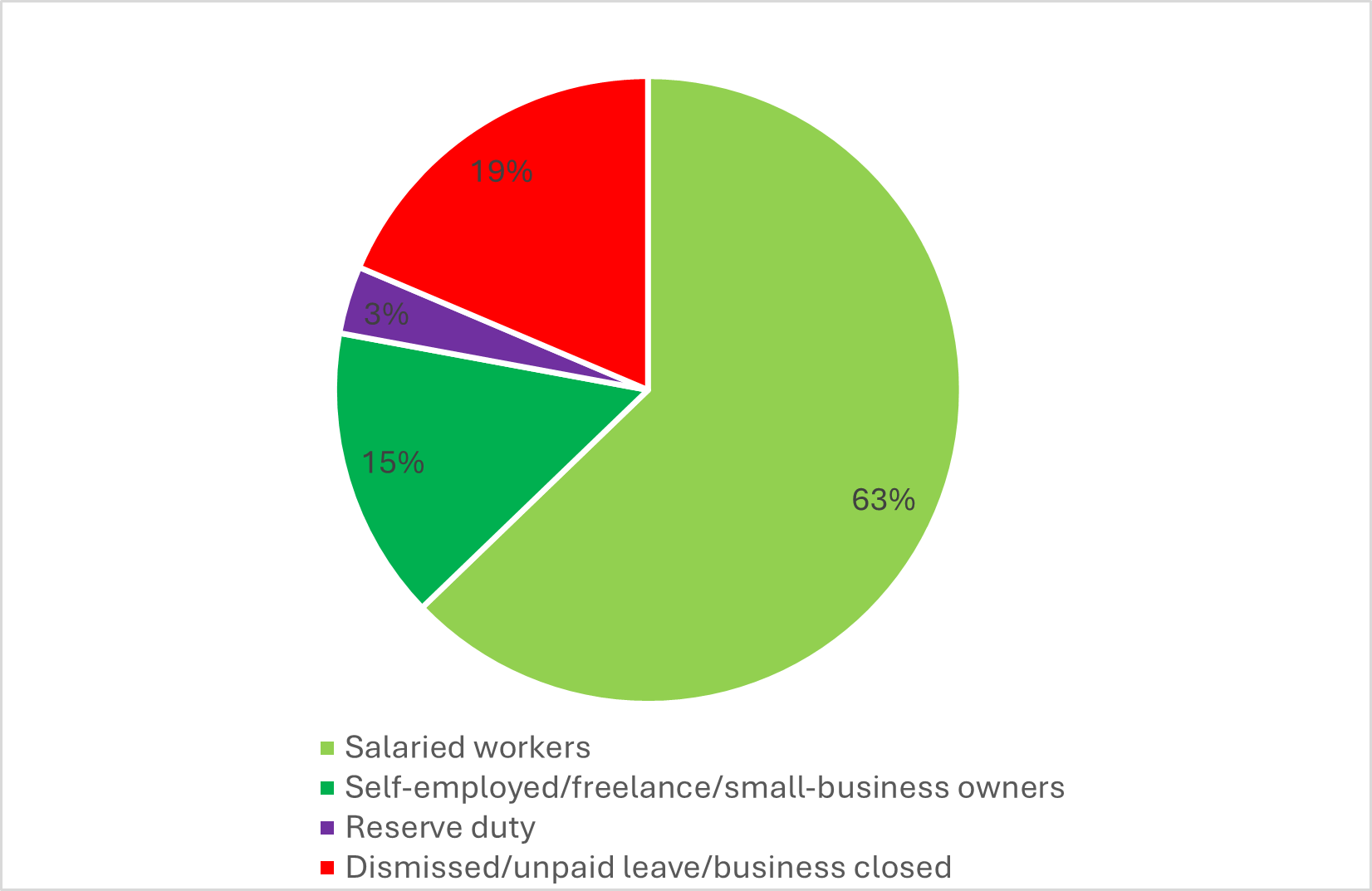

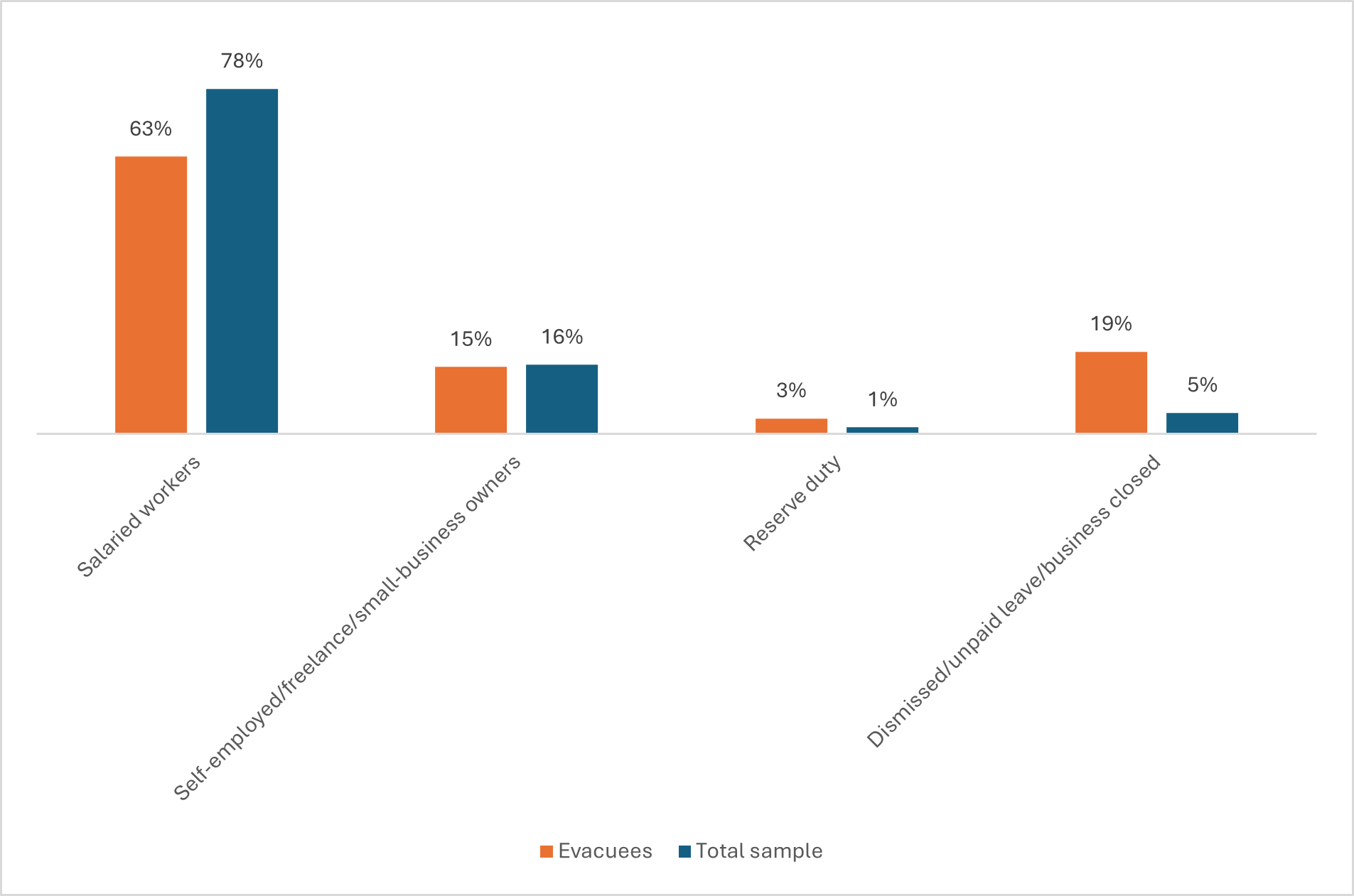

The majority of evacuees who responded to the survey[1] (63%) are currently salaried workers, a lower proportion than in the total sample (78%). Around 15% are self-employed workers, freelancers, or own a company, a similar proportion to the total sample. A notably large share of evacuees (19%) said that at the time of the survey (between December 24 and January 25) they had been dismissed from their job or placed on unpaid leave, or that their business had closed due to the war (among those who had been self-employed), compared to around 5% of the total sample. In addition, around 3% reported that they were in reserve duty.

Figure 3. Current employment status of evacuees who were in employment before the war, January 2025 survey

Figure 4. Employment status of those who were in employment before the war (evacuees compared to total sample)

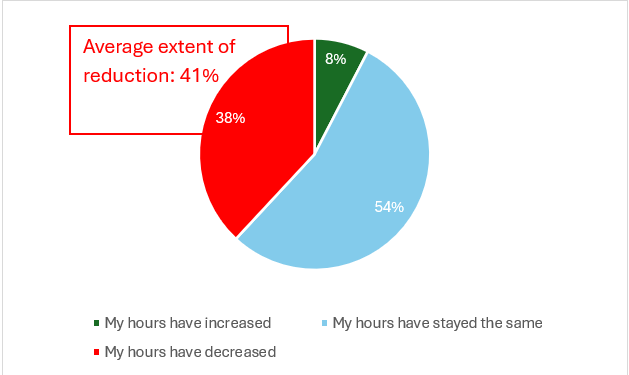

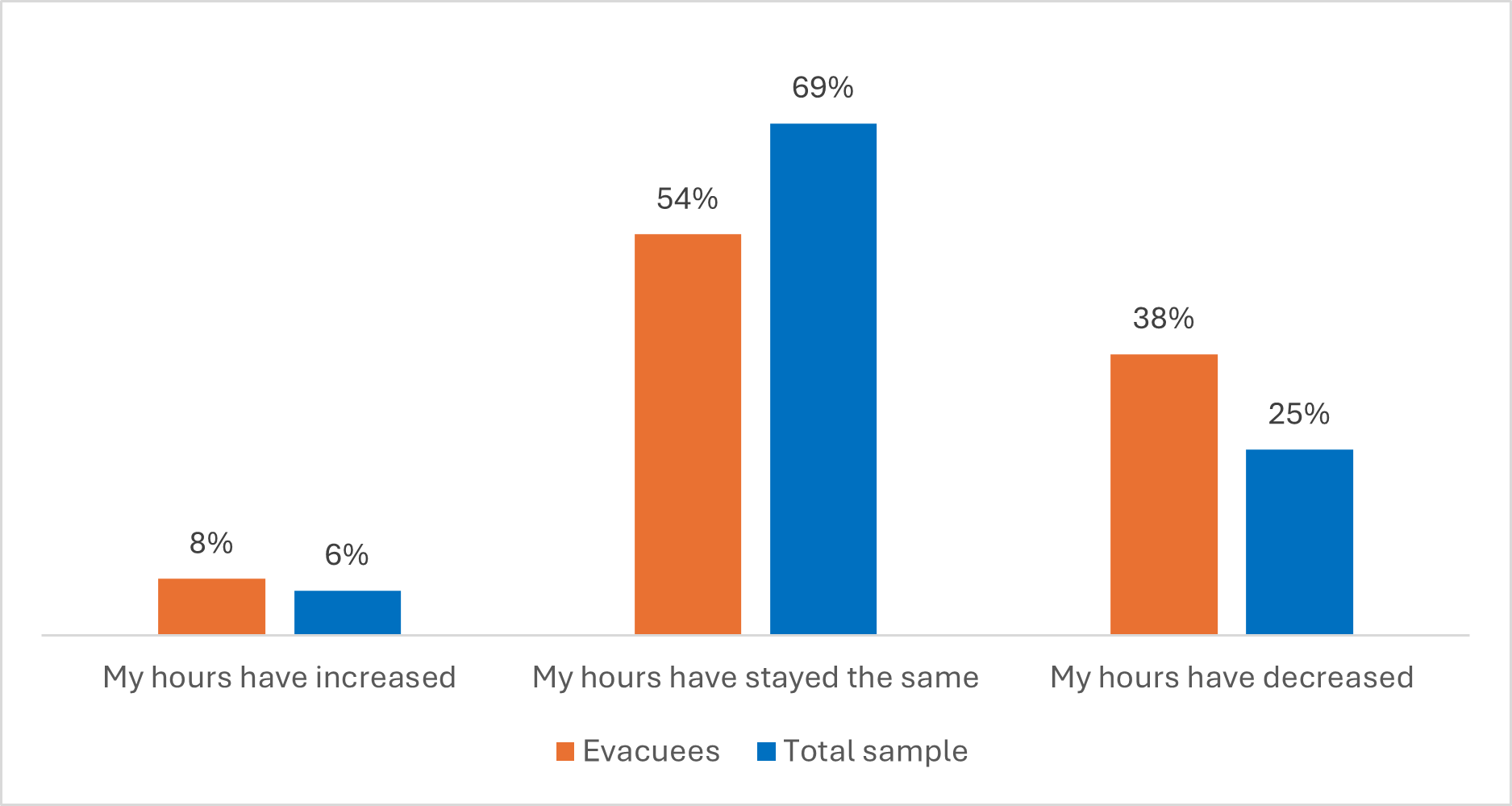

Just over half the evacuees (54%) reported that their work hours had remained unchanged relative to before the war (for self-employed workers, this question related to the scale of their business activity), 38% reported that their work hours/business activity had decreased due to the war, and 8% that their work hours/business activity had increased. Among those who reported a reduction in their number of work hours or scale of business activity, the average size of that reduction was 41%.

Though we received a relatively small number of responses to this question (67), it is worth noting that we found a considerable difference between self-employed and salaried workers in the sample of evacuees. As in the total sample, self-employed workers were hit much harder than salaried workers by the effects of the war: 77% of self-employed/freelance evacuees reported a drop in business activity, compared to just 28% of salaried evacuees who reported a reduction in work hours. Despite the small sample size, we decided to present this finding as it constitutes a very sizable discrepancy, and also because it tallies with the findings in the total sample, where 54% of self-employed workers reported a decrease in business activity due to the war, while just 19% of salaried workers reported a reduction in work hours.

The fact that around 15 months since the outbreak of the war, a majority of self-employed/freelance evacuees are still reporting a decrease in the scale of their business activity due to the war highlights the urgent need to create a clear and ordered mechanism that will provide an immediate response to this population group during emergency situations such as wars, pandemics, and other extreme events that are beyond their control. This should be similar to the existing mechanisms for assisting salaried workers, who in times of crisis are entitled to a security buffer, whether by means of unpaid leave or receiving unemployment benefits.

Figure 5. Impact of the war on number of work hours/business activity among evacuees[2]

Figure 6. Impact of the war on number of work hours/business activity (evacuees compared to total sample)

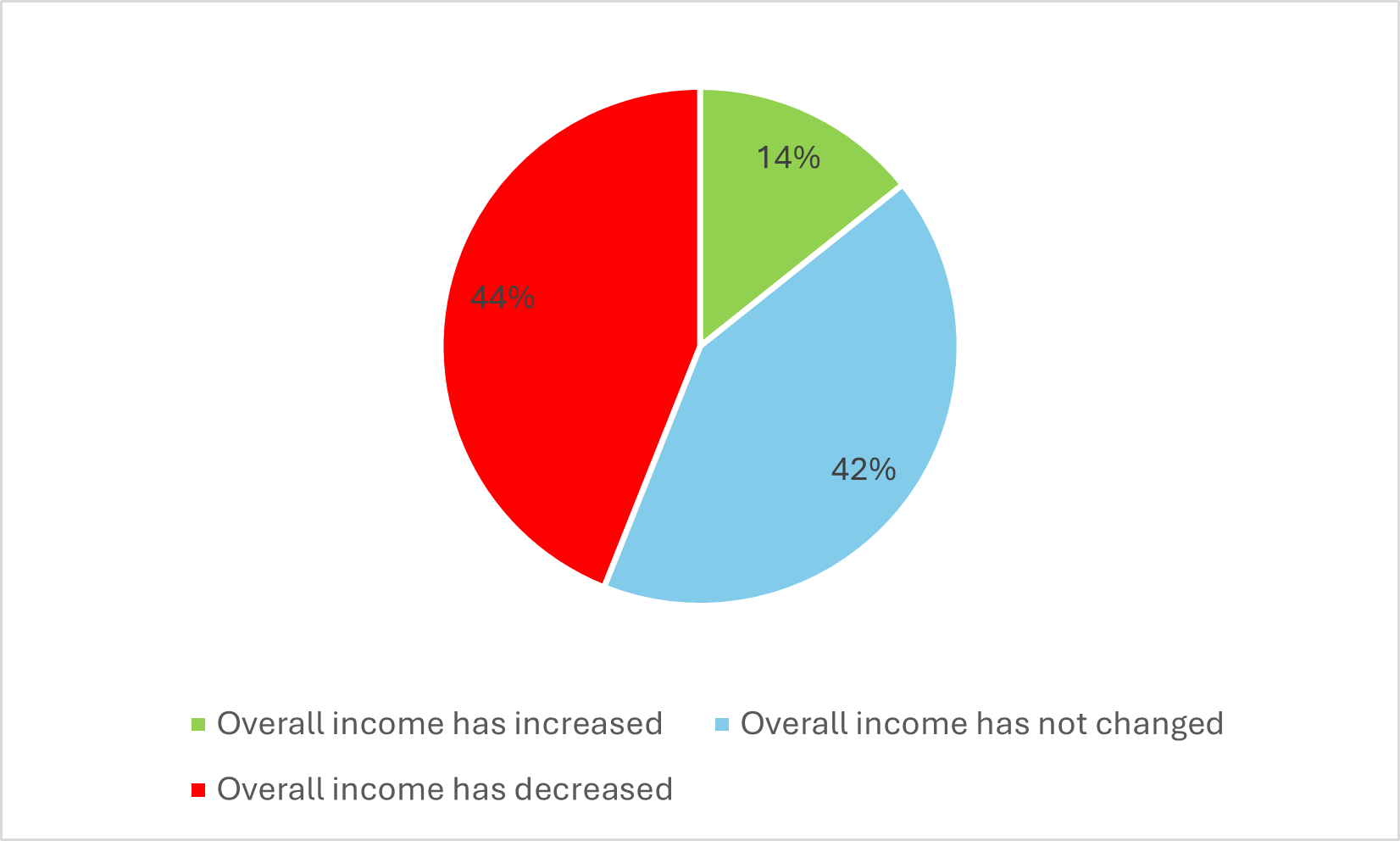

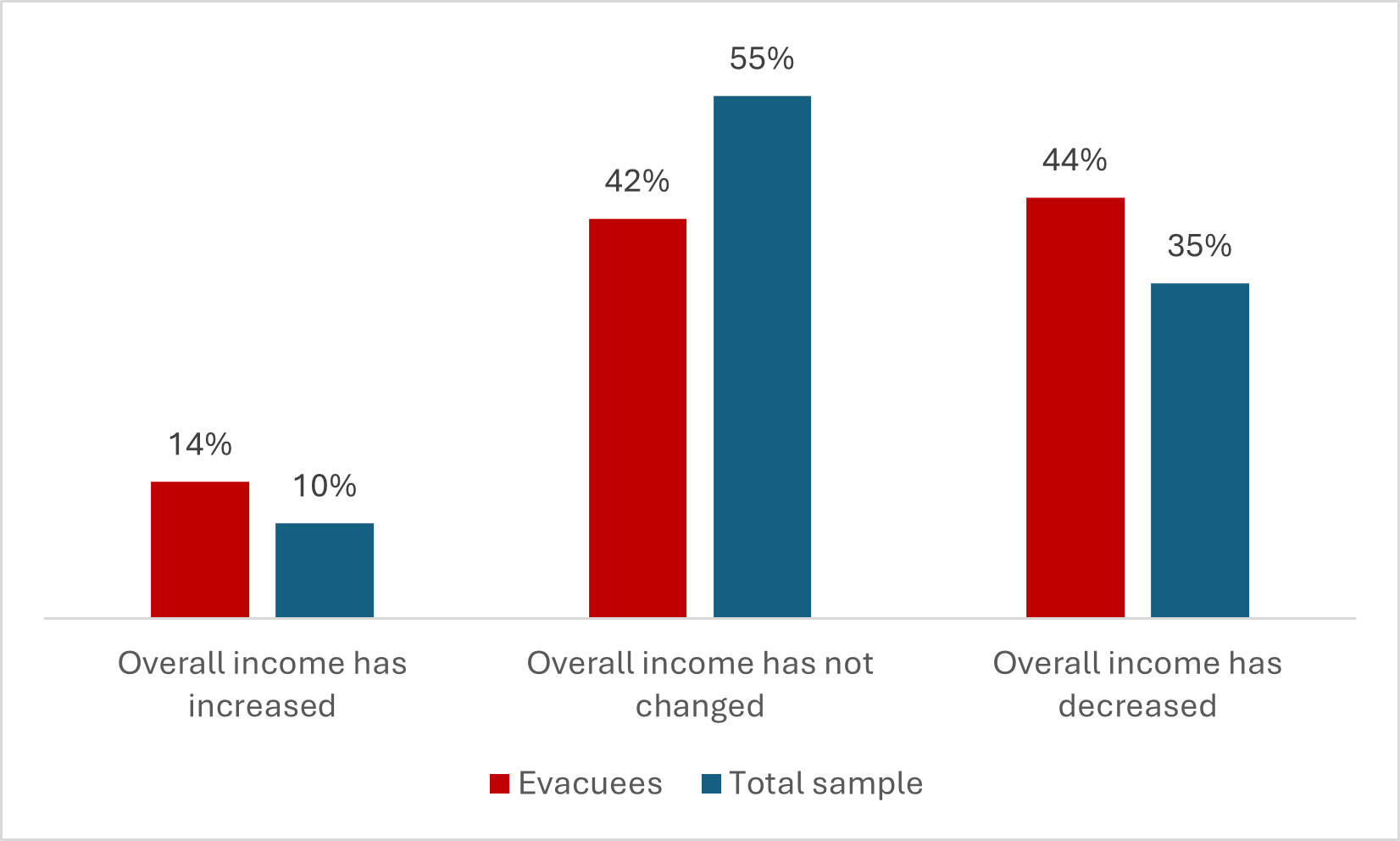

The survey found that 44% of evacuees reported that their household income, at the time they responded to the survey, was lower than before the war. A similar share (42%) said that their household income had not changed, and around 14% reported an increase in their household income since the start of the war.

Figure 7. Change in household income of evacuees relative to pre-war levels

A year and quarter after the outbreak of war, the proportion of evacuees reporting that their incomes were lower than pre-war levels (44%) remained higher than the national average (35%).

Figure 8. Change in household income relative to pre-war levels (evacuees compared to total sample)

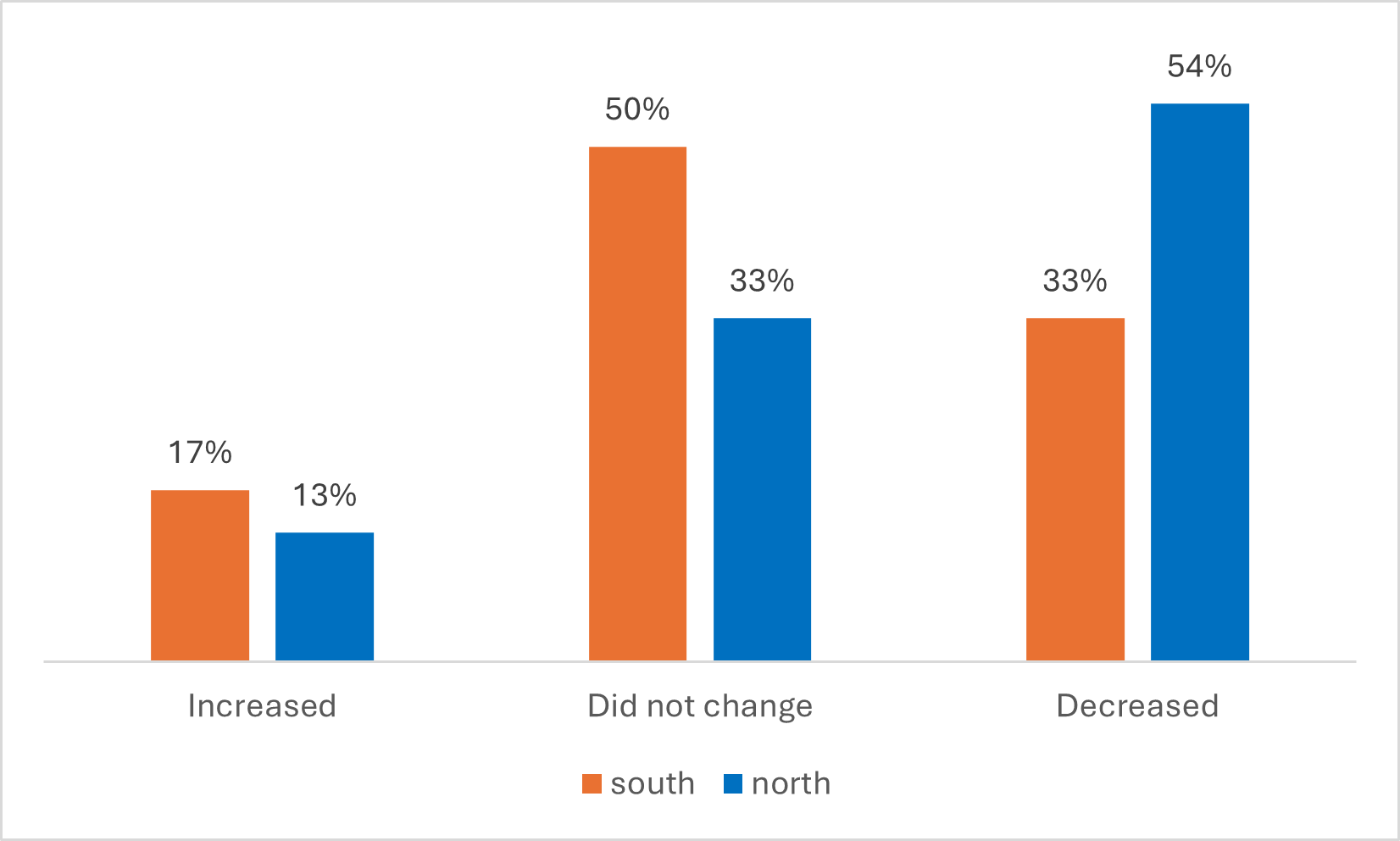

A particularly large share of evacuees from the north (54%) reported a decrease in household income relative to pre-war levels, compared to 33% of evacuees from the south. This picture is reversed when examining the share who reported no change in their incomes since the beginning of the war: Around half the evacuees from the south said that their household income had remained unchanged, compared to around a third of the evacuees from the north.

Figure 9. Change in household income of evacuees relative to pre-war levels (by area of residence)

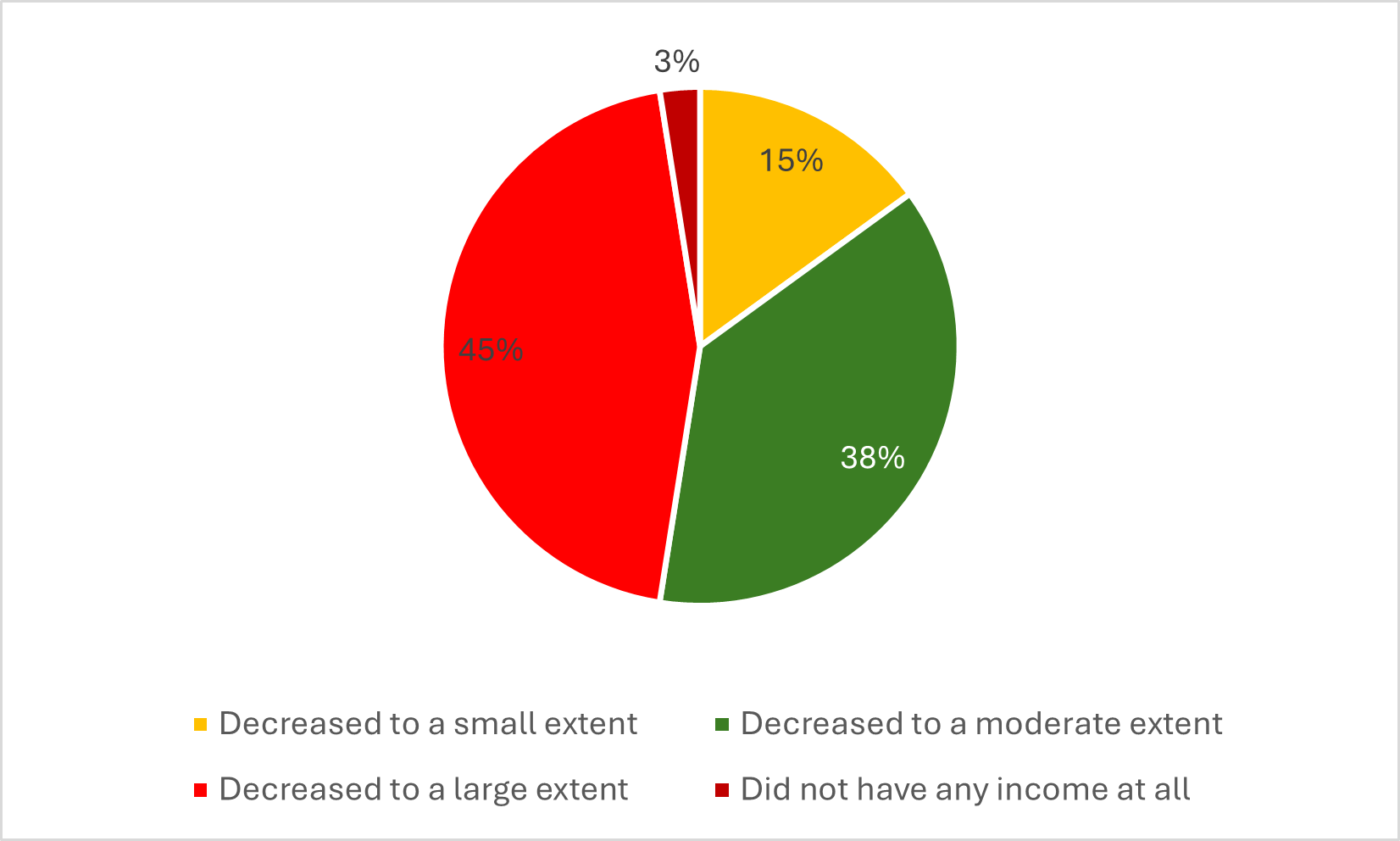

Among those evacuees who reported a decline in their household income, the majority (83%) reported a moderate or large decrease relative to pre-war levels: 45%, a large decrease; and 38%, a moderate decrease. Only 15% reported a small decrease in household income, while 3% said they had no income at all before the war.

Compared to the total sample, the evacuees have suffered a much greater reduction in income. While 31% of respondents in the total sample reported a significant decrease in income, among evacuees the equivalent share stands at 45%. Accordingly, the share of evacuees who reported a small or moderate decrease (15% and 38%, respectively) is smaller than the equivalent share in the total sample (27% and 41%, respectively).

Figure 10. Extent of decrease in household income of evacuees (% of evacuees who reported a reduction in household income relative to pre-war levels)

Figure 11. Extent of decrease in household income (evacuees compared to total sample; % of those who reported a reduction in household income relative to pre-war levels)

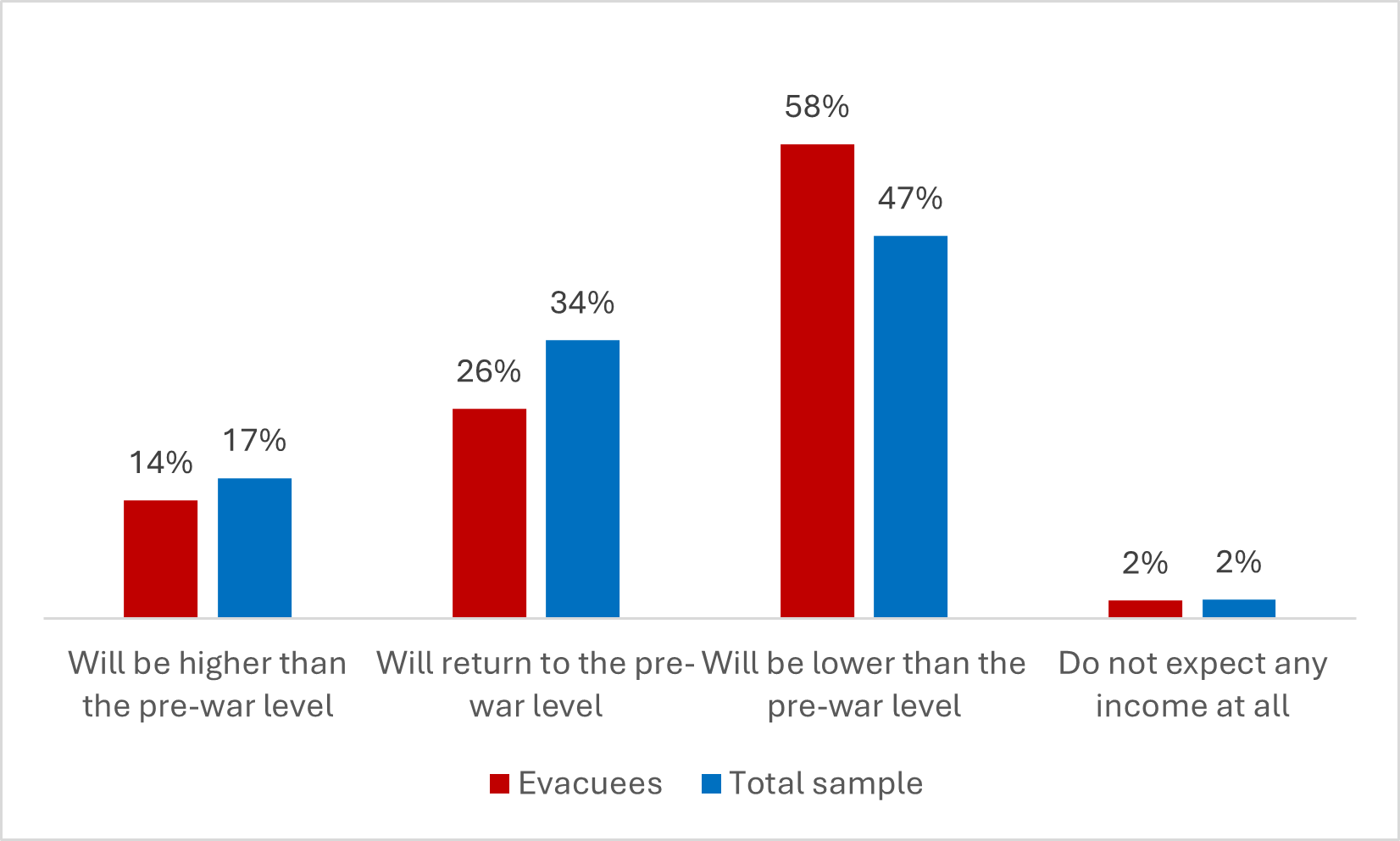

We asked our respondents to estimate what would happen to their household income over the next two months. Around 60% of the evacuees expected their household income in January–February 2025 to be lower than pre-war levels, compared to 49% of respondents in the total sample. Of these, 25% of evacuees expected their income to be slightly lower than before the war, while 33% anticipated that it would be moderately lower or very much lower, compared to 25% in the total sample.

Figure 12. How do you expect your gross household income in January–February 2025 to be different from the equivalent period before the war (January–February 2023)? (evacuees)

On the other hand, around a quarter of evacuees (26%) estimated that their household income in the next two months would return to pre-war levels, compared to 34% of the total sample, while 14% expected their income to be higher than in the equivalent period before the war.

Figure 13. How do you expect your gross household income in January–February 2025 to be different from the equivalent period before the war (January–February 2023)?[3] (evacuees compared to total sample)

It is worth noting here again that the survey was carried out between mid-December 2024 and early January 2025, after the ceasefire agreement with Lebanon but before the current deal for the release of the hostages in Gaza, which also includes commitments to end the war. It is reasonable to assume that these developments would have influenced the interviewees’ general outlook and level of optimism looking toward the future.

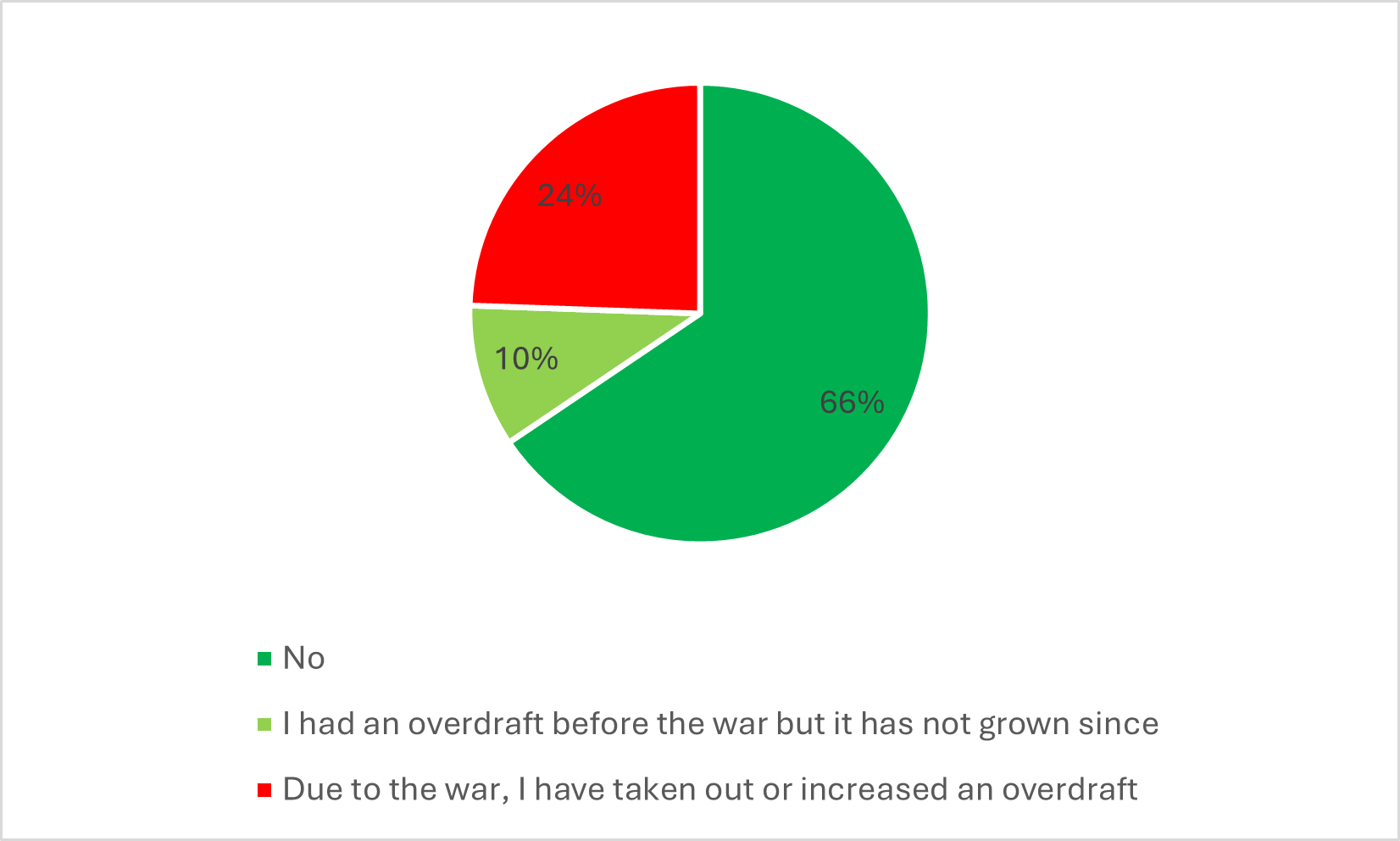

Some two-thirds of respondents to the January 2025 survey reported that they have not taken out an overdraft due to the war. No substantial differences were found between evacuees and the total sample in this regard.

In addition, around 24% of evacuees said that they have taken out an overdraft or increased an existing overdraft due to the war (similar to the equivalent proportion of the total sample), while around 10% had an overdraft before the war which has not grown due to the war. Taking into account the sampling error, we did not find significant differences regarding overdrafts between the sample of evacuees and the total sample.

Figure 14. Has the crisis caused your household to take out or increase an overdraft? (total sample)

Overall, the survey found that the financial situation of evacuees is similar to that of the general population, seemingly as a result of the various support grants given to evacuees. We did find that the financial situation of evacuees from the north is worse than that of evacuees from the south. It is a reasonable assumption that this is related to the difference in the rate of return to their homes between these two groups, and to the larger grants given to evacuees who have already returned home. It is likely that ending the support grants will make it difficult for evacuee households to keep their heads above water.

It is important to remember that that a year ago, at the end of February 2024, the government ended the “repopulation” grants to evacuees from the south whose localities had been declared by the IDF as safe to return to, and those who chose to remain in hotels were entitled to financial assistance until the end of July. Repopulation grants remained in place for localities that were not declared safe. In addition, with the aim of encouraging evacuees from the south to return home, those returning to live in their localities were offered grants that were gradually reduced in size over time.

By contrast, the support grants for evacuees from the north are expected to continue through to the end of February 2025, with evacuation grants coming to an end in March 2025 and one-time return grants being offered instead. The survey data reflect the financial situation of these evacuees before the cessation of government support grants.

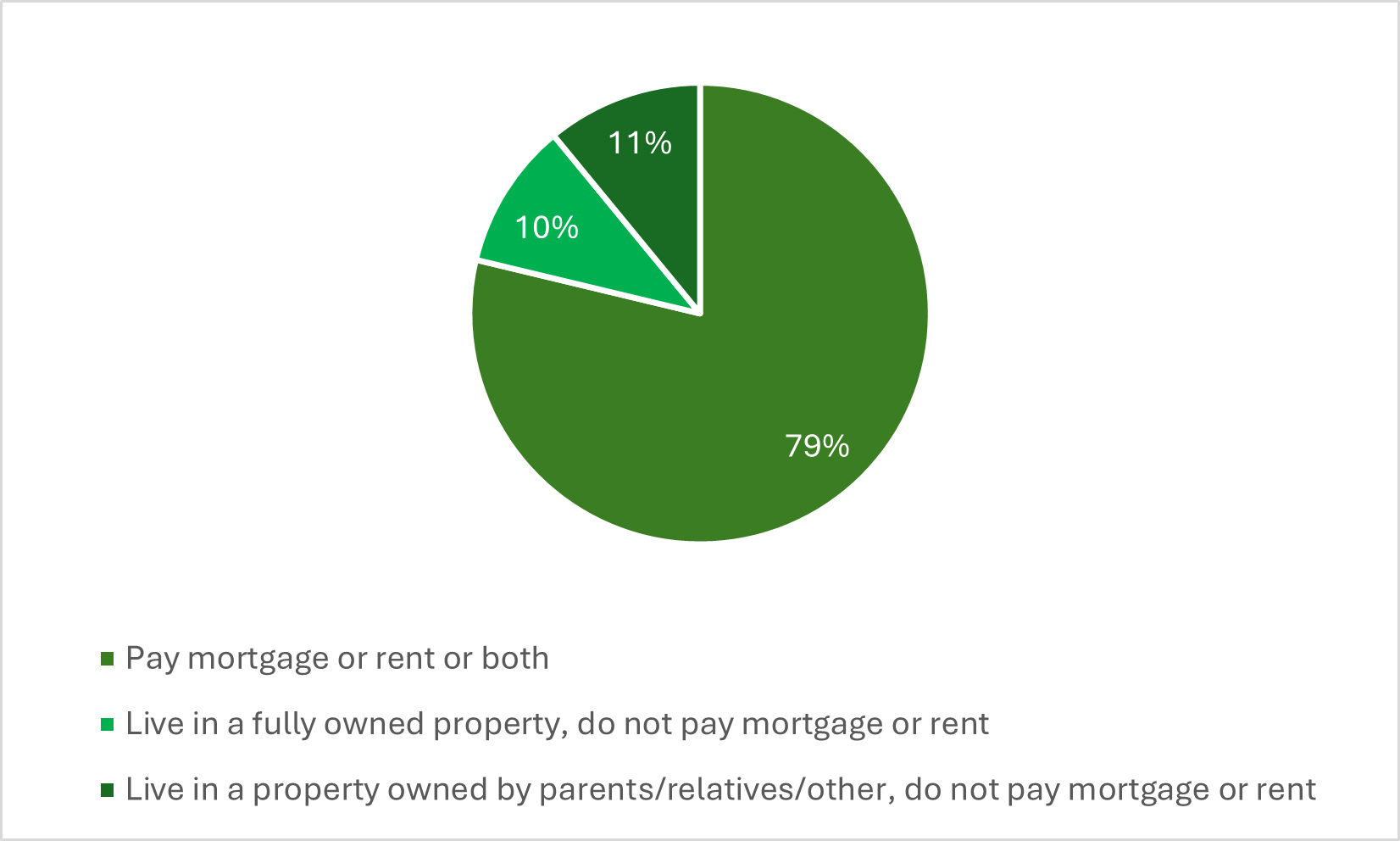

The majority of evacuees (79%) make monthly payments for housing, whether a mortgage or rent, or both. Around 10% live in a property they own fully, and 11% live in a property owned by a relative or other person and do not pay for housing.

Figure 15. What type of payments do you make for housing? (evacuees)

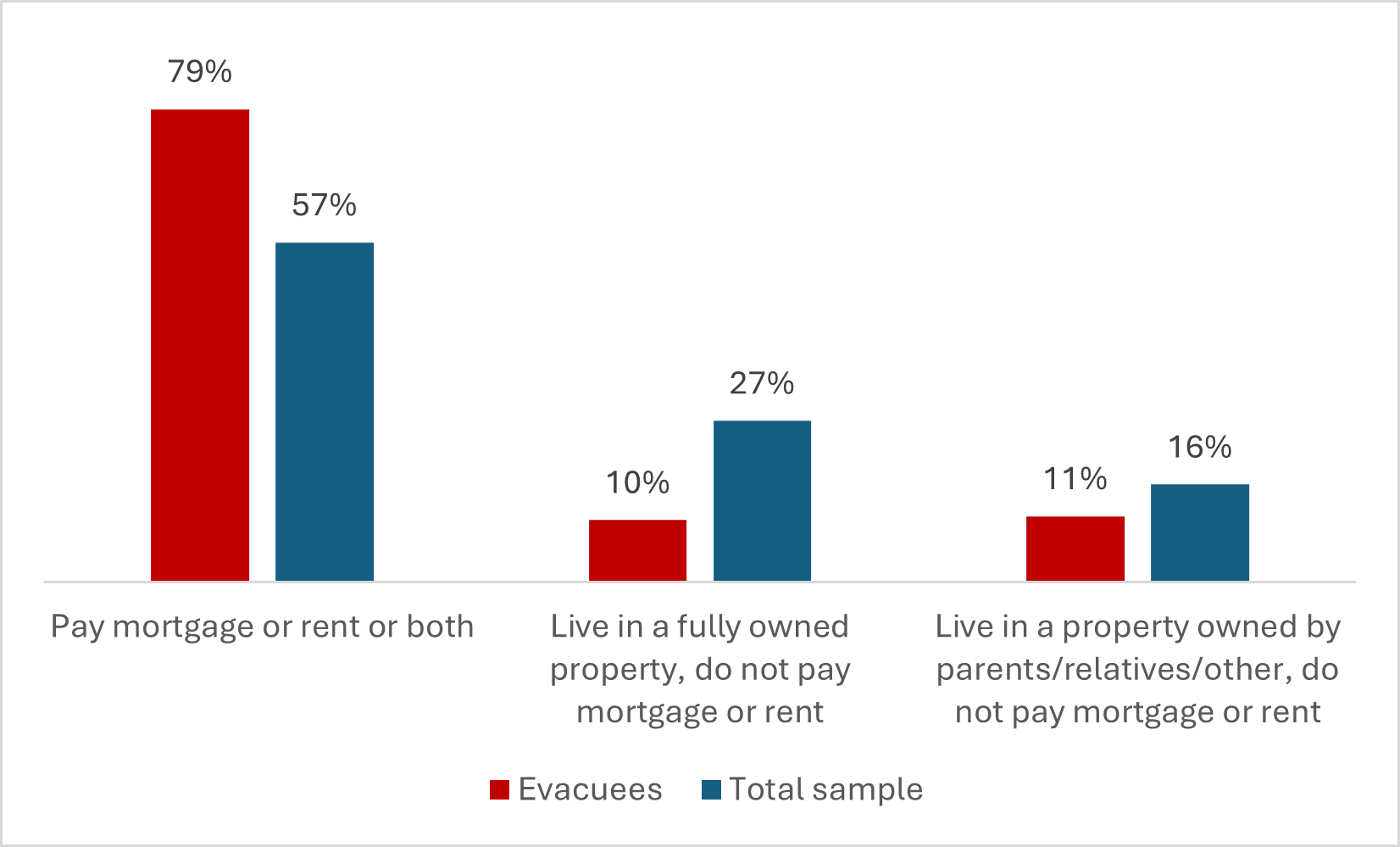

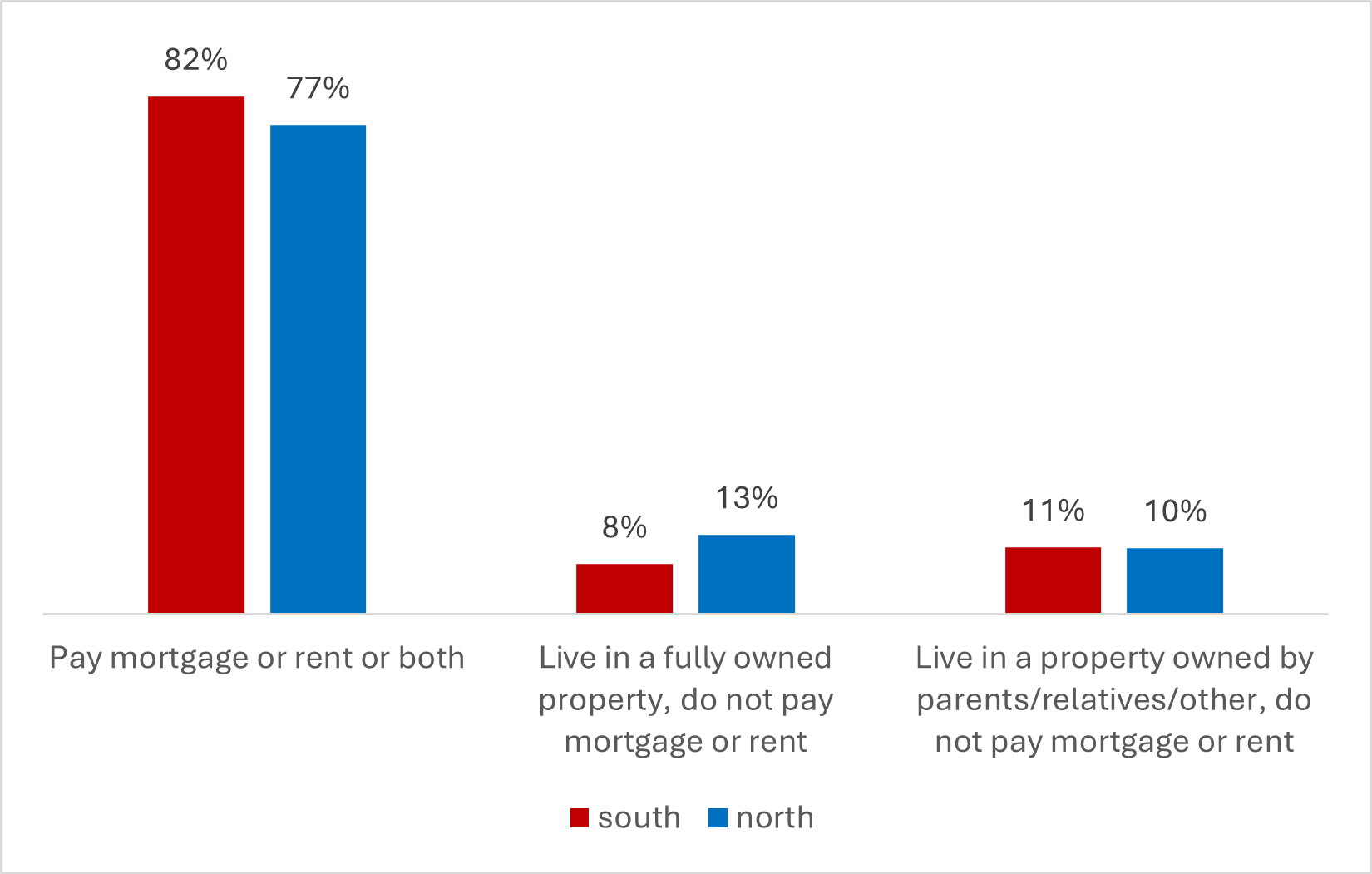

A relatively high proportion of evacuees pay mortgage and/or rent payments (79%), compared to the total sample (57%). Accordingly, a lower proportion of evacuees live in a property they own fully (10%), compared to 27% of respondents in the total sample. We did not find significant differences in this regard between evacuees from the north and evacuees from the south.

Figure 16. What type of payments do you make for housing? (evacuees compared to total sample)

Figure 17. What type of payments do you make for housing? (evacuees, by area of residence)

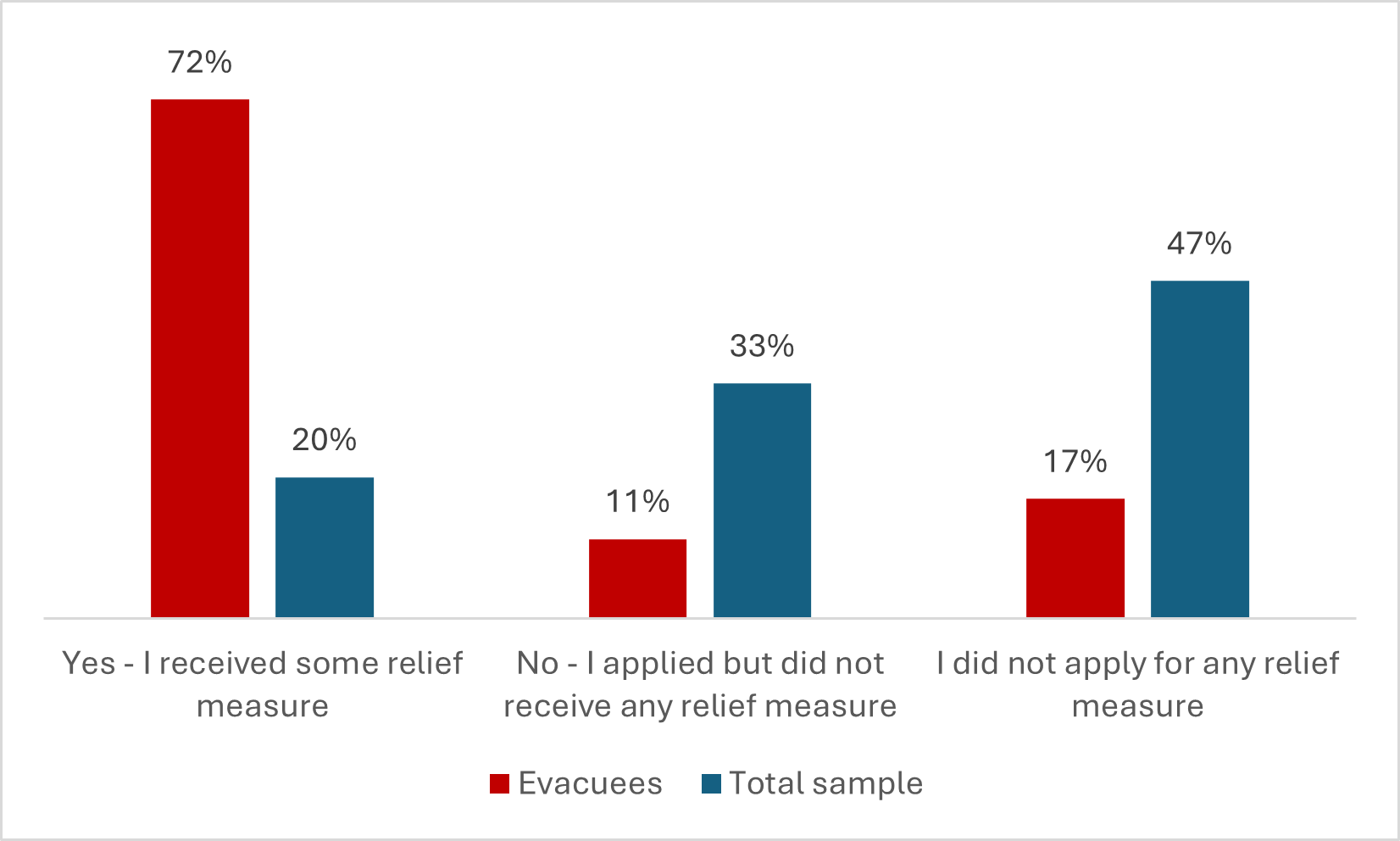

Regarding leniency on payments for housing (mortgage or rent), we found a sizable difference between evacuees and the general population, with around 72% of evacuees having received some kind of leniency on their housing payments, compared to just 20% of respondents in the total sample. Moreover, while only 11% of evacuees reported having requested some form of leniency and not receiving it, the equivalent share of the total sample was around a third. This may explain the more difficult financial circumstances of certain population groups, such as Arabs and the self-employed, who have found themselves in financial difficulties as a result of the war but have not been granted the leniency they expected from the banking and/or financial system. Among evacuees, a relatively small percentage (17%) did request any kind of leniency, compared to a much larger share of the general population (47%).

Figure 18. Have you received any kind of leniency on housing payments, such as rent or mortgage payments? (evacuees compared to total sample; % of those who are struggling to meet their housing payments)

[1] This survey sampled only respondents who were working at the time the Iron Swords war broke out.

[2] Due to the small number of respondents, it is not possible to present a breakdown of evacuees from the south compared to evacuees from the north

[3] Respondents to the January 2024 survey were asked about their income in January-February 2024.